The maritime industry's fuel transition is often framed as a technology challenge. Which fuels will emerge as the preferred pathways to decarbonisation? How quickly can production scale? What infrastructure will be required to support adoption?

These questions matter. But a new report, ‘Building the sustainable maritime fuel supply chain’, by the Lloyd's Register Maritime Decarbonisation Hub (The Decarb Hub) suggests there is another question the industry should be asking, which is: where will those fuels come from?

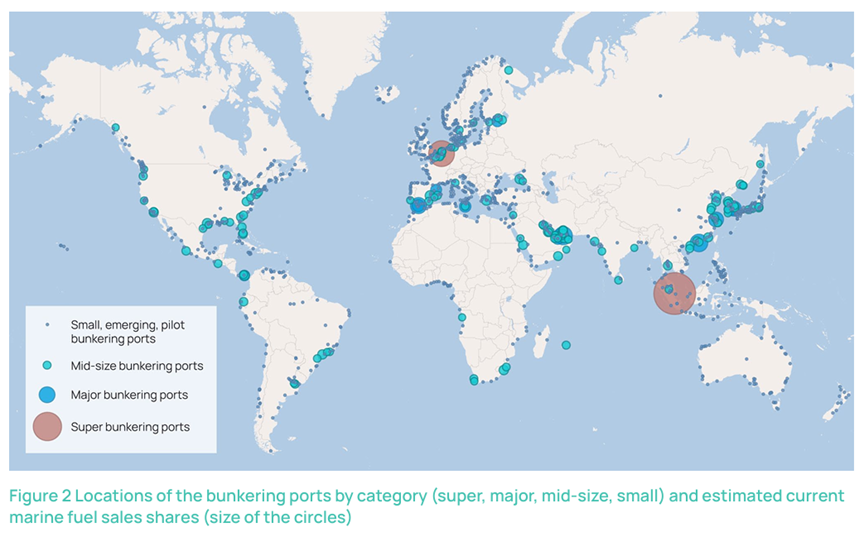

For more than a century, marine fuel supply has been concentrated around a relatively small number of locations. Today, around half of the world's marine fuel is sold in just 19 ports. Singapore alone accounts for roughly a quarter of global bunkering volumes. This new report suggests that emerging bunkering hubs may challenge assumptions about how sustainable fuel markets develop.

Global bunkering demand remains highly concentrated. Around half of global marine fuel demand is concentrated in just 19 ports, creating focal points for early sustainable fuel deployment and infrastructure investment.

Yet when The Decarb Hub mapped credible sustainable fuel projects against today's bunkering landscape a different picture emerged. Of the ports linked to potential future fuel supply, 82% sit outside today's top-tier bunkering hierarchy.

Future fuel supply may emerge outside today's dominant bunkering hubs. Most ports linked to credible sustainable fuel projects are not currently among the world's leading bunkering centres, highlighting the need for new supply-chain connections between production regions and demand hubs.

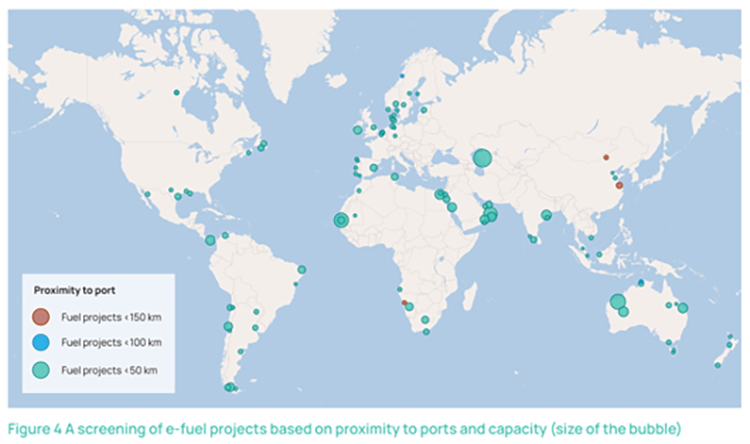

Emerging e-fuel supply is concentrated in a small number of strategic export gateways. At least 127 e-fuel projects with credible maritime export potential were identified, clustering strongly around regions in Australia, Middle East, Europe, and coastal industrial hubs across Asia, Africa, and America, with 63% of projects already co-located within existing industrial facilities.

Sustainable biofuel projects cluster in established production regions and can build on existing bunkering infrastructure. 87 selected biofuel projects (65 bioethanol, 11 biomethanol, and 11 biomethane) were identified mainly across Europe, North America, APAC and Brazil, pointing to 51 potential fuel distribution ports that can act as early, lower-risk entry points for the maritime fuel transition.

This finding highlights a geographic puzzle at the heart of shipping's fuel transition: the places best suited to produce sustainable fuels are not typically the places ships buy fuel today.

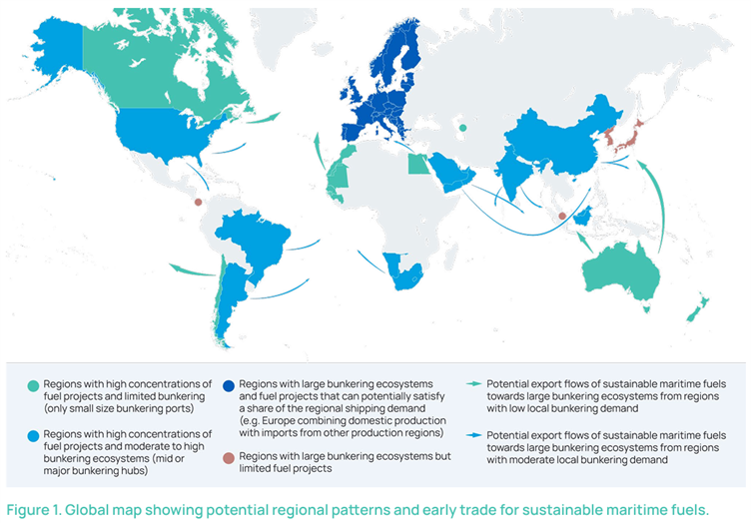

And the reasons are straightforward. Future fuel production is shaped by access to renewable energy, industrial ecosystems, feedstocks, and export infrastructure. Demand for those fuels, meanwhile, remains concentrated around current major shipping hubs and established trade routes. In the medium-to-long term, bunkering patterns may shift significantly.

For example, production capacity is emerging in Australia, the Middle East, India, parts of Southeast Asia, Atlantic Africa and South America, while major bunkering demand remains concentrated in locations such as Singapore, Europe, Japan and Korea.

For Carlo Raucci, Director of Sustainable Fuels and Strategy at the Decarb Hub, this shift has implications that extend beyond fuel production. “Fuel access is the next frontier of equitable ocean governance,” he argued in a recent commentary for Observer Research Foundation.

The challenge, he suggests, is not simply producing new fuels. It is ensuring that the benefits of the transition are distributed across a broader set of regions and stakeholders than today's energy system. The report's findings suggest this may already be happening.

Many of the emerging fuel nodes identified in the analysis are not traditional bunkering centres but production gateways where ports connect to industrial clusters, renewable resources and export infrastructure. This dynamic could play an important role in future maritime energy trade.

And this distinction matters because it changes how the industry should think about fuel and other supply chains. Sustainable fuels may need a new relationship between production regions and demand centres. Early trade could develop along green energy corridors, connecting emerging production locations with established maritime demand.

Ports become key connection points, linking national energy transition and local co-benefits with global shipping demand for clean fuels. According to Raucci, “This transition is about more than new fuels. It's about building a resilient maritime energy system."

This is why the report places particular emphasis on the readiness of relevant infrastructure. Building supply chains requires coordinated investment across production, storage, transport and bunkering. It also means identifying which locations are best positioned to play different roles within those networks.

Industrial ecosystems will be particularly important, the research suggests. Around 63% of credible e-fuel projects assessed are under development within existing industrial facilities, while most of the remainder are found close to established industrial or port energy clusters.

Developers seem to prioritise infrastructure, expertise, and market access alongside proximity to renewable resources. This reinforces a broader lesson from the report, that shipping's fuel transition is not only about producing low-carbon fuel, but also about systems.

First mover port authorities, fuel producers, shipowners and financiers need to identify the trade routes, partnerships and supply-chain connections that link production to demand.

Importantly, the report does not predict winners. Its findings are screening-level hypotheses intended to help a wide range of stakeholders from port authorities and terminal operators, bunker suppliers and fuel producers, shipowners and cargo interests, financiers, to policymakers, to prioritise where further investigation and collaboration may be most valuable.

Findings suggest that the geography of future maritime fuel supply could look markedly different from the one the industry knows today.

The transition to sustainable fuels is often described as a change in what ships burn. The emerging evidence suggests it will change where maritime energy is produced, traded and distributed – and who gets to participate in that future.

Read the full ‘Building the sustainable maritime fuel supply chain’ report

Maritime System in Transition

The Decarb Hub's ‘Maritime System in Transition’ series explores decarbonisation, resilience, and the future of global shipping and is part of the Fuel Adoption Programme. This series is designed to give decision-makers the evidence and frameworks needed to accelerate a credible, well-sequenced maritime energy transition.

‘Building the sustainable maritime fuel supply chain’ is the first publication in the series. Future publications will build on this foundation, examining how infrastructure, finance, fleet, and policy can come together to create a coherent and resilient system.

The Decarb Hub is an independent, not-for-profit system intervention platform established through a partnership between Lloyd's Register Foundation and Lloyd's Register Group. Through coalitions, research, and systems-focused programmes, the Hub accelerates the sector's transition towards a decarbonised shipping industry with human safety and sustainability at its core.

Learn more about The Decarb Hub